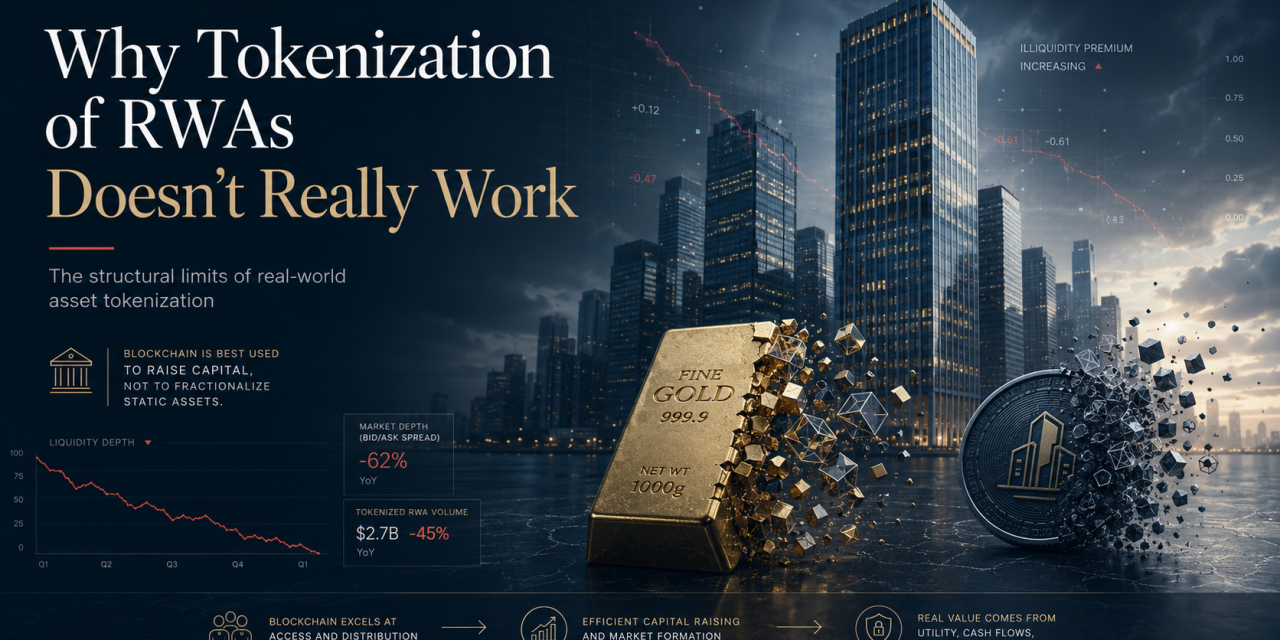

The Core Thesis of Real World Asset Tokenization

The prevailing market enthusiasm for real-world asset tokenization fundamentally conflates the tracking of physical assets with the mechanics of capital raising. The core thesis extracted from contemporary market analysis indicates that the foundational mathematical models supporting the fractionalization of static assets fail to align with the operational realities of debt service, liquidity, or market yield.

The true market opportunity does not reside in tokenizing existing physical properties or commodities, but rather in leveraging blockchain infrastructure to execute highly efficient capital raising activities through digital equity and smart contracts. The conflation of these two distinct activities has generated significant consternation and confusion within the digital asset sector.

Furthermore, classifying cryptocurrency assets as functional currencies is a structural misnomer; the sector operates predominantly as a speculative market where investors acquire assets at 10 cents with the expectation of an appreciation to a dollar, rather than utilizing the asset to buy a cup of coffee.

To achieve institutional-grade capital efficiency, the focus must pivot from the mathematically unviable fractionalization of static assets toward the deployment of compliant digital registries for corporate fundraising.

The Mathematical Bottlenecks of Real Estate Fractionalization

Structural bottlenecks severely limit the viability of real estate tokenization. A primary argument advanced by operators for property fractionalization is the theoretical reduction of debt service; however, the underlying mathematical framework fails to support this mechanism:

• Consider a residential asset with a theoretical valuation of a million dollars, carrying an active mortgage balance of 600,000 to 700,000, and requiring a fixed payment of $5,000 a month.

• Executing a fractional sale of 30% of this asset yields $300,000 in capital.

• Unless that $300,000 is directly utilized to completely amortize the loan, the monthly debt service remains exactly $5,000 a month.

• Whether the property owner owes 600,000 or 6,000, the payment obligation does not decrease until the principal is entirely paid off.

The token price in these real estate fractionalization models remains anchored strictly to the net asset value of the underlying property. While investors in speculative digital assets historically target massive exponential growth, real estate appreciation typically yields 5%, 8%, 10%, or 20% in a year. Consequently, real estate tokens cannot mathematically generate the outsized returns expected by digital asset investors without artificial market manipulation driving up the token value based on hype.

Applying these exact mathematical models to commercial real estate, such as a 10-million-dollar apartment building, yields identical operational constraints:

• Investors acquiring fractional tokens in a 10-million-dollar apartment building receive no percentage of the rent collected, equating to zero dividend yield.

• Investors exercise no governance or control over if or when the underlying building is sold.

• Investors face severe market liquidity constraints when attempting to exit their fractional positions, as there is no guaranteed secondary market for these specific tokens when market dynamics shift or COVID impacts tenancy.

Even attempting to fractionalize high-profile trophy properties, such as the Empire State Building, fails to resolve these fundamental mathematical and liquidity limitations. The fractionalization provides liquidity to the original property owner without altering the structural debt obligations or providing tangible operational yield to the token holder.

The Indivisibility and Liquidity Constraints of Physical Commodities

The tokenization of physical commodities, explicitly gold, introduces deep structural bottlenecks regarding physical redemption, custody, and divisibility. Operators frequently assert that token holders maintain direct ownership of the underlying physical gold housed in secure vaults; however, this architecture ignores the practical indivisibility of the physical asset. The majority of traditional gold investors do not hold physical assets, but rather digital certificates representing fractional ownership of a larger asset held by a third party. The introduction of blockchain tokens fundamentally mirrors this existing digital certificate model without solving the physical constraints of the commodity:

• A standard bank bar of gold is a specific unit of measure historically valued at seven or eight or $900,000, or a million dollars.

• If a retail or institutional token holder allocates exactly $4,857 to a tokenized gold platform, there is no viable operational mechanism to represent that exact fraction in physical delivery, as it is physically impossible to shave corresponding fractions off a bank bar.

• If an investor holds a 1-ounce gold coin valued at $5,000 and requires $250 for an immediate transaction, there is no physical method to fractionalize that solid coin to extract the exact required liquidity.

The market opportunity fundamentally breaks down when digital fractionalization collides with physical indivisibility. The structural promise of tokenized physical assets is an illusion when the asset itself cannot be dynamically partitioned to meet real-time liquidity demands.

Macroeconomic Currency Fluctuation and The Stablecoin Misnomer

The classification of gold-backed or treasury-backed digital assets as stablecoins fundamentally misrepresents the volatility inherent in macroeconomic currency fluctuation risk. The assertion that a gold-backed token is inherently stable is structurally flawed; gold experiences persistent price volatility, often fluctuating more significantly than the US dollar over weekly or monthly intervals. While gold may serve as a functional investment hedge against long-term inflation, it lacks the absolute pricing stability required for a functional corporate medium of exchange.

The operational distinction between retail transactions and institutional capital deployment highlights this specific bottleneck:

• A consumer might easily purchase a $3 cup of coffee or a $30 meal internationally with minimal impact from minor currency valuation shifts.

• Conversely, executing a corporate acquisition for a 30-million-dollar coffee company introduces massive currency fluctuation risk, necessitating complex hedge and arbitrage strategies to mitigate exposure.

• Currencies are not valued equally; a million pesos does not equal a million US dollars, and valuations against fiat currencies like the real or the AED fluctuate constantly.

Technological upgrades to settlement infrastructure do not eliminate underlying asset volatility. Digital payment systems operate on superior technological rails, analogous to a 240 miles per hour magnetic levitation train functioning in jurisdictions like China. Traditional financial rails, including Swift, Fedwire, and ACH, are the equivalent of 1800s steel rails. However, regardless of whether the technological infrastructure utilizes 1800s steel rails or advanced magnetic levitation rails, the base assets being transported still fluctuate. A stablecoin tied to US treasuries or the AED will still experience continuous value fluctuations, invalidating the concept of absolute pricing stability for corporate transactions spanning 10, 20, or $30 million.

Capital Formation Versus Asset Tokenization: Resolving Regulatory Conflation

The most significant structural bottleneck in the digital asset sector is the persistent conflation of existing real estate tokenization with pre-sale capital formation. During an industry conference in São Paulo, Brazil, operators claimed to achieve a 30% return on real-world asset projects. Upon strict analytical review, these returns were not generated by fractionalizing an existing building, but by executing pre-sales for new construction projects. This activity is unequivocally a capital raising endeavor, equivalent to issuing an equity investment, a direct investment, or a SAFE agreement.

Labeling capital formation as real-world asset tokenization triggers severe regulatory misalignment.

By designating construction fundraising as tokenization, operators attract unnecessary scrutiny from banking regulators who mistakenly perceive the assets as competing digital currencies. The primary utility of blockchain in these institutional scenarios is not tokenizing a static asset, but deploying highly efficient technological rails to raise capital. Whether a corporation seeks capital through a public listing governed by the SEC and FINRA, a private equity round, or a digital tokenization event, the core structural activity remains capital formation. The regulatory bottlenecks arise exclusively from the terminology utilized and the failure to structure these capital raises under appropriate legal frameworks.

The Strategic Value Unlock Digital Equity and Operational Leverage

The true value unlock for blockchain infrastructure rests entirely in operational leverage for corporate capital formation, supply chain tracking, and digital equity distribution. Rather than attempting the unviable fractionalization of static real estate or physical commodities, institutions must concentrate on migrating physical asset tracking and capitalization tables to transparent digital infrastructure.

The concept of migrating physical assets to the blockchain is functionally equivalent to the historical expansion of Internet Protocol parameters. The implementation of IPv6 was designed to circumvent the exhaustion of DNS and domain registrations, establishing the foundational architecture for IoT devices and Wi-Fi tracking.

Similarly, placing an asset like a car on a digital smart contract registry allows for superior governmental and consumer tracking compared to archaic paper or Excel registries. However, registering a vehicle on a smart contract does not constitute tokenization for the purpose of selling fractional ownership; it is strictly a tracking mechanism.

When applied to corporate capital formation, this exact technological upgrade resolves critical structural bottlenecks. Under traditional frameworks, an angel investor allocating capital to an early-stage software development company receives archaic documentation: a physical piece of paper functioning as a term sheet and an opaque entry on an analog spreadsheet that cannot be independently verified. There is no tactically, legally, or electronically binding mechanism continuously tracking that early-stage investment.

Under the US JOBS Act, crowdfunding capital is already a legally established practice

However, it is a standalone process missing a technical integration. The use of a digital smart contract would then seamlessly integrates with blockchain technology to facilitate digital equity fundraising. Companies can utilize existing legal frameworks—such as the JOBS Act, Regulation A, and Regulation CF—to raise capital by issuing equity directly onto a digital smart contract or blockchain certificate.

This process replaces archaic, opaque tracking methods like paper term sheets and analog spreadsheets with a transparent, legally binding digital record. By issuing equity through a smart contract, it functions as a superior structural and legal document for early-stage angel investors, giving them concrete, verifiable proof of their investment and a reliable way to track it. Ultimately, leveraging the JOBS Act allows companies to conduct highly efficient, legally compliant capital formation rather than issuing unregulated tokens or speculative cryptocurrencies.

Deploying blockchain as a capital formation tool resolves this systemic inefficiency. By utilizing compliant frameworks such as the JOBS Act, Regulation A, or Regulation CF in the US, institutions can issue digital stock certificates directly via smart contracts for crowdfunding capital.

This transition replaces fragmented, analog capitalization structures with transparent, legally binding digital registries. The strategic implementation of digital equity dramatically increases operational efficiency, legal transparency, and institutional trust for early-stage investors. The ultimate strategic mandate for the sector is to abandon the mathematically flawed tokenization of indivisible real-world assets and fully capitalize on the structural advantages of compliant digital equity capital formation.

{kind=link}